Traditional IRA vs Roth IRA

Retire

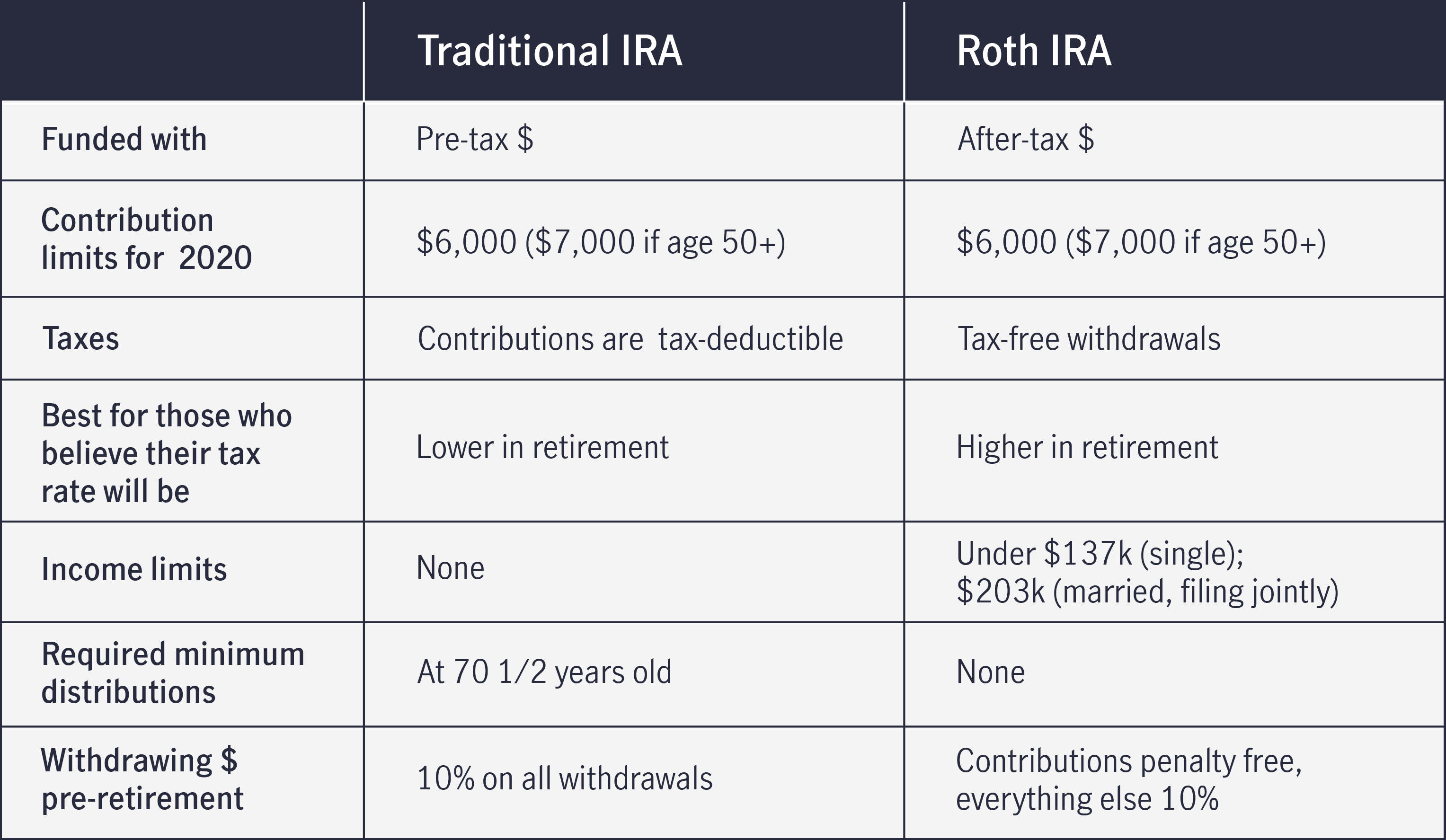

Individual Retirement Accounts (IRAs) can be a great option for retirement savings — as either a primary source or a supplement to a work-sponsored plan (like a 401(k)). Two of the most common IRAs are the Traditional and Roth IRA.

Both are available to anyone over the age of 18, allow a maximum contribution of $6,000 annually ($7,000 if over age 50)¹, and allow you to withdraw money at any time (although, you may pay penalties and taxes on the money if you’re under 59½).

Before choosing one over the other, there are tax differences and income limits you should be aware of.

What is a Traditional IRA?

It’s a retirement plan that you contribute pre-tax money into. Pre-tax means you’re not taxed on your contribution the year you make it. For example, if you make $60,000 a year and contribute the maximum of $6,000 to a traditional IRA, your taxable income for the year will be $54,000.

Your tax deduction can however be limited if you also have a workplace retirement plan. And if you file taxes as a single person making between $65,000-$75,000, you can only take a partial tax deduction. (See how the IRS determines your deduction eligibility here.)

All of your contributions grow tax-deferred until you take the money out in retirement. Once you begin making withdrawals, you’ll pay taxes on that money at whatever your current tax rate is.

A traditional IRA is usually a good choice if you expect to be in a lower tax bracket in retirement because you’ll pay fewer taxes when you withdraw the money. However, it’s important to note that you are required to take minimum distributions at age 72 (if you were born after June 30, 1949) or age 70½ (if you were born before July 1, 1949). ² If you have earned income, you can continue making contributions regardless of your age.

What is a Roth IRA?

With a Roth IRA, you contribute post-tax dollars, meaning you pay the taxes upfront in the year you contribute. Your contributions are not tax-deductible, but you can take withdrawals of your contributions at any time (penalty and taxfree).³ Also, the earnings on your contributions will generally be tax-free in retirement when you make qualified withdrawals.⁴

There are income limits to be aware of. For example, if you’re a single income household and you make more than $139,000, you can’t contribute to a Roth IRA at all. (You’ll find the full list of contribution limits at the IRS website here.)

And unlike a traditional IRA, you’re never required to take minimum distributions from your Roth IRA if you originally opened the account.

Quick Comparison Chart - Contribution limits for 2020

Tax penalties for early withdrawals

To dissuade you from taking money out before retirement, in most cases, the IRS penalizes you for withdrawals before the age of 59½. Typically, there’s a 10% early withdrawal tax if you don’t qualify for an exception.

Under a traditional IRA, the early withdrawal tax applies to the withdrawal of your contributions and earnings. Plus, the money you take out is counted as income for the year, so you’ll pay income taxes on top of the 10% fee.

Unlike a traditional IRA, the early withdrawal tax penalty does not apply to the withdrawal of your contributions to a Roth IRA but will apply to the earnings portion of the withdrawal.

Choose the IRA that’s right for you

To recap, a traditional IRA typically gives you an immediate tax benefit at time of contribution, but you’ll pay taxes on that money (and earnings) when you make a withdrawal (most likely, at a lower tax bracket.). With a Roth IRA, there is no upfront tax advantage, but you’ll pay no tax on the earnings on your contributions⁵ when you make qualified withdrawals.⁶ No matter which you choose, you can feel good knowing you’ve taken a great step in planning for your future and a retirement lifestyle on your terms.

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

Citations:

1 Contributions to a Roth IRA may be limited based on an individual’s income and tax filing status. Annual limits are based on the IRS 2020 Contribution limits and are subject to change.

2 Under the CARES Act, required minimum distributions (RMD) for 2020, including any delayed 2019 RMD (if the 2019 delayed RMD was not taken prior to January 1, 2020), have been waived and are not required to taken.

3 In this document, all tax disclosures regarding Roth IRA contributions are limited to the federal income-tax code and, in particular, all references to tax-free treatment of qualified distributions are intended to refer to the treatment of such distributions at the federal level only.

4 Qualified withdrawal or distribution from a Roth IRA (including the 5-year rule)—A qualified withdrawal or distribution from a Roth IRA is a payment made afer the Roth IRA account owner atains age 59½ (or afer death or disability) and afer the Roth IRA has been established for at least 5 years. In general, in applying the 5-year rule, count from January 1 of the year the first contribution was made to the Roth IRA. Roth IRA owners should contact their financial or tax advisor for specific details on the 5-year rule and whether any special rule may apply.

5 In this document, all tax disclosures regarding Roth IRA contributions are limited to the federal income-tax code and, in particular, all references to tax-free treatment of qualified distributions are intended to refer to the treatment of such distributions at the federal level only.

6 Qualified withdrawal or distribution from a Roth IRA (including the 5-year rule)—A qualified withdrawal or distribution from a Roth IRA is a payment made afer the Roth IRA account owner atains age 59½ (or afer death or disability) and afer the Roth IRA has been established for at least 5 years. In general, in applying the 5-year rule, count from January 1 of the year the first contribution was made to the Roth IRA. Roth IRA owners should contact their financial or tax advisor for specific details on the 5-year rule and whether any special rule may apply.

Financial planning and investment advice provided by John Hancock Personal Financial Services, LLC (“JHPFS”), an SEC registered investment adviser. Investments: not FDIC insured – No Bank Guarantee – May Lose Value. Investing involves risk, including loss of principal, and past performance does not guarantee future results. Diversified portfolios and asset allocation do not guarantee profit or protect against loss. Nothing on this site should be construed to be an offer, solicitation of an offer, or recommendation to buy or sell any security. Before investing, consider your investment objectives and JHPFS’s fees. JHPFS does not provide legal or tax advice and investors should consult with their personal legal and tax advisors prior to purchasing a financial plan or making any investment.